#5things: Before The Bell

Data dump, tariff-exposed stocks, Dell slumps, retail round up

Yesterday we were in crisis mode. I needed to sign the kids up for summer camp. In November. Imagine my shame when I realized I haven’t mapped out what every single week of July and August will look like…by November 26th. This is why parents are not okay!

Data dump: Futures are mixed and bonds are rallying as we get a data dump from the US ahead of their holiday tomorrow. We just got a second read of GDP that showed the economy expanded 2.8% in the third quarter (as expected). While consumer spending was revised down to 3.5% from 3.7%, that is still the best pace of growth all year. This comes as consumer confidence is at a 16-month high in the US. Can’t say the same for Germany and France. German consumer confidence came in below all estimates and unexpectedly dropped in France. American exceptionalism continues. “The European continent continues to look like a basket case,” wrote Andrew Brenner of NatAlliance in a note to clients. He says that is the reason we are seeing a rally in US bonds today. Note we will get the Fed’s preferred measure of inflation this morning, but not until 10amET (normally 8:30amET). Timing is wonky because of the pending US holiday tomorrow.

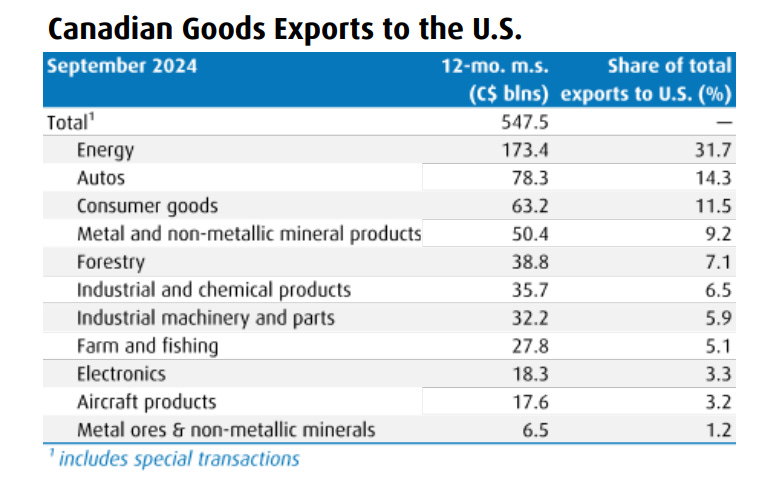

Doing the math: The S&P 500 advanced for a 7th straight day, while the TSX fell flat as investors sold shares in companies with exposure to higher tariffs. While many strategists said this could be just a negotiating tool, investors weren’t waiting around the find out. In the US, shares of GM and Ford took a hit due to their manufacturing exposure in Mexico. Bombardier, BRP and Linamar were the biggest losers on the TSX because of manufacturing and tariff concerns. On a sector basis, energy was one of the biggest drags. However, many note that it is difficult to replace Canadian crude at US refineries and driving up the cost of energy would hit American pocketbooks. Nevertheless, as BMO points out in the chart below, the energy sector is the most exposed to higher tariffs. The folks at TD Cowen put together a list of names that could be negatively impacted assuming all tariffs go through and there are no mitigating factors (a big assumption). I included the list at the bottom of today’s note.

Dull: Shares of Dell are down nearly 12% on weak PC sales. While it beat profit expectations, total sales were weaker as PC sales dropped 18%. HP Inc’s results also showed similar sluggishness in the PC recovery. Dell’s sales and profit outlook was also below expectations. Dell is up about 60% from the August low because of momentum in its AI server business. Sales in this unit spiked 58% from last year and management said demand shows no signs of slowing down. They saw record AI server order demand. However, the strong momentum is at odds with the results. AI server sales are up from last year, but down from the last quarter. Most analysts say this is just “lumpiness” in demand. Clearly investors are not keen to take their lumps.

Striking out: Investors are taking profit in cyber-security company CrowdStrike this morning. Results were better than expected across the board but the profit forecast was a little light. The company also removed a distributor from their annual recurring revenue numbers which meant the new forecast was below expectations. HSBC downgraded the stock because of limited visibility into annual recurring revenue. However, Morgan Stanley remains bullish saying it was “prudent” to bring down the ARR forecast because estimates were too high. Sales crossed $1 billion for the first time which will bring comfort to investors following what the company calls the “July 19th incident”. Recall, that is when the company updated its software in a routine upgrade and then caused a near global computer crash. The stock crashed along with it, dropping as much as 44% over the next few weeks before bottoming in August. That proved to be a great buying opportunity. It is up nearly 70% from the August low.

Retail roundup: Shares of Guess? Inc are poised to open at a 2-year low, down about 9% in the pre-market. Sales increased 13%, but this was less than expected. Profit was below expectations. The retailer is also cutting its sales and profit forecast for the year because of a “challenging environment” in North America and Asia. On the flip side, shares of Urban Outfitters are surging after sales and profit grew more than expected. Analysts are mostly neutral on the stock, but this morning Citi is upgrading to buy calling the story “too good to ignore.” Citi points out that we are seeing positive momentum at Urban Outfitters stores for the first time in years and its other brands Anthropologie and Free People remain in “solid positions.” They’ve got a street-high price target of $59/share which implies 30% upside.

Bonus: Notable Call from TD Cowen

Names potentially at risk:

o Aritzia

o SpinMaster

o BRP

o Bombardier

o Auto parts: Linamar, Magna, Martinrea

o Ag Growth, Mattr and Russel Metals

o KP Tissue, Western Forest Products, West Fraser Timber, Interfor

o On the positive side: financials could benefit from deterioration in Canadian dollar in particular BMO, Manulife and Sunlife

o Nutrien

o CN Rail and CPKC

o Converge and Softchoice

Keep up the good work. Very interesting stories to stat my day