In the Money: 5 things to know

Futures mixed, tariffs hurt, BCE earnings, Great-West beats, Peloton pops

My kids have started to include “writing the newsletter” into their imaginative play. My daughter just explained to my son that she can’t play with him because “she needs to get the newsletter out.” My son responded by propping up his own “computer” and telling her to shut the door until he is done. The only difference between their play and our real life is that she actually listened to him.

A new episode of In the Money with Amber Kanwar is out now! I spoke with Martin Pelletier of TriVest Wealth about why preservation of capital is just as important as growing capital. He shares his three best investing ideas including why he took profits on Suncor which reported last night. Tune in on Apple, Spotify, or here. YouTube will be out this afternoon.

Mixed: We are drinking from a firehose of earnings this morning with stocks wrestling to control the tone of the tape this morning. Futures are mixed as we’ve got nearly 40 companies on the S&P 500 reporting and 10 reporting on the TSX. We saw a late day surge in the markets yesterday, which swept the TSX to a gain of more than 1% on the day. In particular there was a late day surge for BCE and Rogers while tech stocks ripped. We saw nearly +10% moves in Celestica and BlackBerry. From a macro perspective, we got a Bank of England rate cut that was expected but with a surprising twist that two of nine governors would have preferred steeper rate cuts. Yesterday, US Treasury Secretary Scott Bessent made headlines when he said the Trump administration isn’t going to harp on the Fed to cut rates. Instead they will focus on lowering 10-year treasury yields. They plan to do this by increasing oil production, which should lower inflation and rein in the budget deficit. Despite the remarks, the US 10-year is actually selling off a bit here. Earnings from Qualcomm (-4%) are putting a damper on the tech sector after the world’s biggest seller of smartphone chips warned that smartphone sales are expected to be flat this year.

Tariff trouble: Despite all the tariff anxiety, the TSX is actually slightly outperforming the S&P 500 year-to-date. However, today Bombardier and Ford are stark reminders that the prospect of a trade war are very real. Bombardier reported a drop in fourth quarter profit, slower revenue growth than anticipated, and warned it could not provide a financial forecast for this year because of the threat of tariffs. “The lack of any 2025 guidance items, while understandable given the current circumstances, will likely disappoint the market…” wrote Cameron Doerksen of National Bank. He is sticking with his buy rating even as the stock has fallen more than 20% since its October high. “Absent tariffs, we continue to see meaningful upside for the stock supported by positive business jet end market conditions and solid free cash flow generation through the end of the decade,” he wrote. Meanwhile, shares of Ford (-5%) are poised to open at a four-year low because it cut its profit forecast by $2 billion in part because of potential new tariffs on Canada and Mexico. The automaker is taking a hit on several fronts: dialing back its efforts when it comes to making electric vehicles, expecting an industry-wide drop in car prices, and a sharp uptick in warranty repair expenses. Sadly, I own this one and it has not been a road to success so far.

Dropping hints: BCE beat analyst expectations in the fourth quarter but warned that profit was going to fall between 8-13% as subscriber growth fell 56% from last year. On the plus side, the company said free cash flow will be higher and maintained its dividend. This has been a key point of anxiety for investors with a dividend yield of 11%. Special shout out to Maher Yaghi at Scotia who pointed out the language about BCE’s dividend opens the possibility of reviewing it before the end of 2025. In particular, BCE included this paragraph about the dividend:“BCE’s common share dividend and common share dividend payout policy will continue to be reviewed by the Board. In its review, the Board will consider the competitive, macroeconomic 8 and regulatory environments as well as progress being made on our strategic and operational roadmap.” This was not in any of the other quarterly press releases in 2024. On our third episode of In the Money with Amber Kanwar, John Zechner and Frances Horodelski said they were buyers. You can watch it here with insights on Bell at 18:30.

Go west: Watch shares of Great-West Lifeco at the open after the insurer reported better than expected earnings. Profit increased 15% and its return on equity was stronger than forecast. It is prompting TD Cowen’s Mario Mendonca to upgrade the stock to buy. “Raising estimates and upgrading to BUY on stronger ROE outlook, accelerated asset gathering at Personal Wealth and, importantly, GWO's lower risk profile in period of uncertainty,” he wrote in a note to clients. Recall, Scotia upgraded Great-West on the back of tariff uncertainty a few days ago with a similar call that it was a good place to hide out.

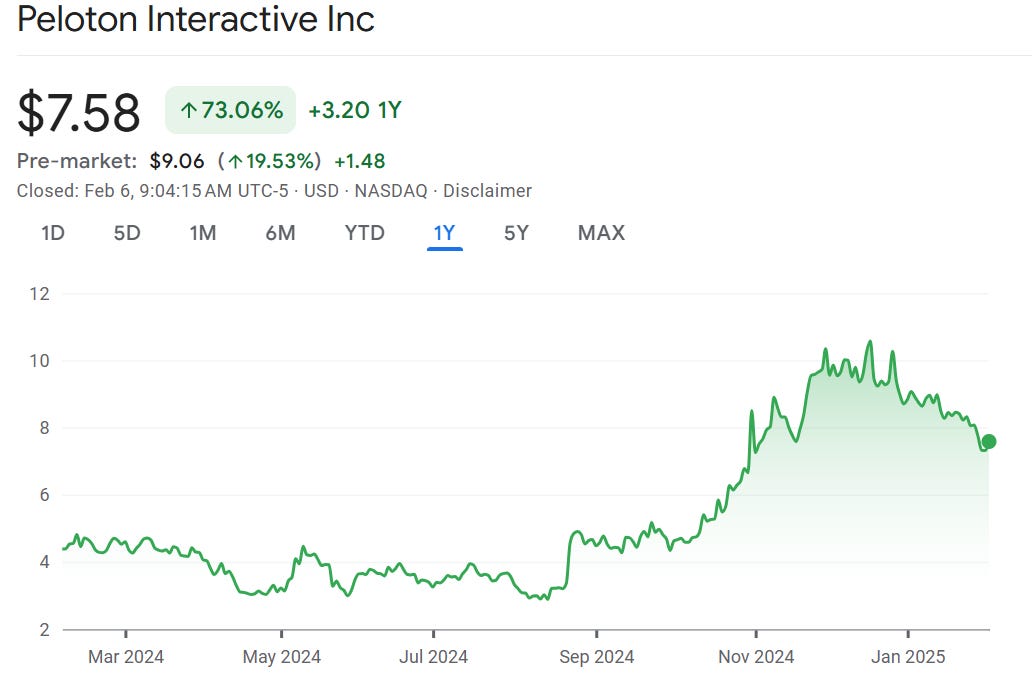

Sweat, baby, sweat: Peloton is ripping higher in the pre-market (+20%) after the embattled bike and treadmill-maker reported a better measure of adjusted profit thanks to cost cuts. The news is overshadowing a forecasted drop in sales that is much worse than anticipated. Peloton was a pandemic darling and is down 95% from the 2021 high. However, over the past year the stock has surged 73%. Recall, in our very first episode of In the Money with Amber Kanwar, Eric Jackson of EMJ Capital picked Peloton as one of his best ideas. You can revisit the episode here with Peloton thoughts at 49:00. Shares of Under Armour is surging 8% on a similar story to Peloton. It is warning that sales will drop 10% this year but boosted its profit forecast on reduced discounting. Under Armour is in the midst of a turnaround under its returning CEO Kevin Plank who came back in April after several years of under performance. The stock is down nearly 70% since the pandemic peak and has its fair share of bears, nearly 17% of the shares outstanding are betting against the company.

I don't know how, but I managed to buy Peloton at the very bottom, shortly after my marriage therapist wife of 50 years insisted on upgrading to the newer bike. She started during Covid. She hates exercise, but loves Cody so it's been a daily routine now for the past 4 years. Product is great, but how long can the new management maintain the magic? When do I sell?