In the Money: 5 Things to Know

Fed day, Keyera's big deal, Aurora Cannabis big miss, Marvell shines, UBS downgraded

Late.

In this episode of In the Money with Amber Kanwar, CI Global Asset Management’s Peter Hofstra shares why he believes the worst of tech sector volatility is behind us and why he remains optimistic on AI. He points to strong and steady spending in the space as a sign that fundamentals are intact, and explains why AI adoption is now a “use it or fall behind” moment for investors and businesses alike. While he uses puts to manage risk when valuations run high, Hofstra makes it clear: right now, he sees more opportunity than downside.

Fed day: Futures are drifting higher this morning as investor attention shifts away from war in the Middle East to the Federal Reserve’s interest rate decision this afternoon. The Federal Reserve is widely expected to keep rates on hold but today’s decision will also come with the “dot plots” - projections by Fed members on where they see interest rates going. Fed days under Jerome Powell have been become a little worse in recent meetings as investors become increasingly disappointed with the lack of rate cuts (see chart below courtesy of Bespoke Investment Group). As of right now the market is pricing in two rate cuts with an October cut fully priced in. A reminder US markets are closed tomorrow to commemorate Juneteenth so we will have a delayed next-day reaction to the Fed decision. Turning to the war between Iran and Israel, tensions remain high with Iran not backing down. The risk premium is showing up in crude with oil trading at $75/bl, the highest since January. Interestingly, gold has not benefitted from a flight to safety with bullion down three sessions in a row albeit still near record highs. The twin combination of higher energy and gold prices have help to support the TSX near all-time highs.

Pipe dreams: Keep on eye on Keyera after announcing plans to acquire all the Canadian assets of a US pipeline company. Keyera will be buying the Canadian natural gas liquids business from Plains All American Pipeline for $5.15 billion. Keyera will be financing the deal, in part, by issuing stock at $39.15/share (a 7% discount to yesterday’s close). Keyera calls this a transformational acquisition that significantly expands their infrastructure across Canada. Keyera says after the deal the company’s enterprise value will be $19 billion from $13 billion presently. BMO is upgrading the stock partly because of the acquisition. “We are upgrading KEY to Outperform from Market Perform following YTD underperformance (~540bps vs. peers and worst performing), the scale-changing $5.15B NGL Plains acquisition, and attractive pro forma valuation of ~9.5x 2026E EV/EBITDA (vs. peer average ~11x),” wrote BMO’s Ben Pham. He sees 30% upside in shares from here.

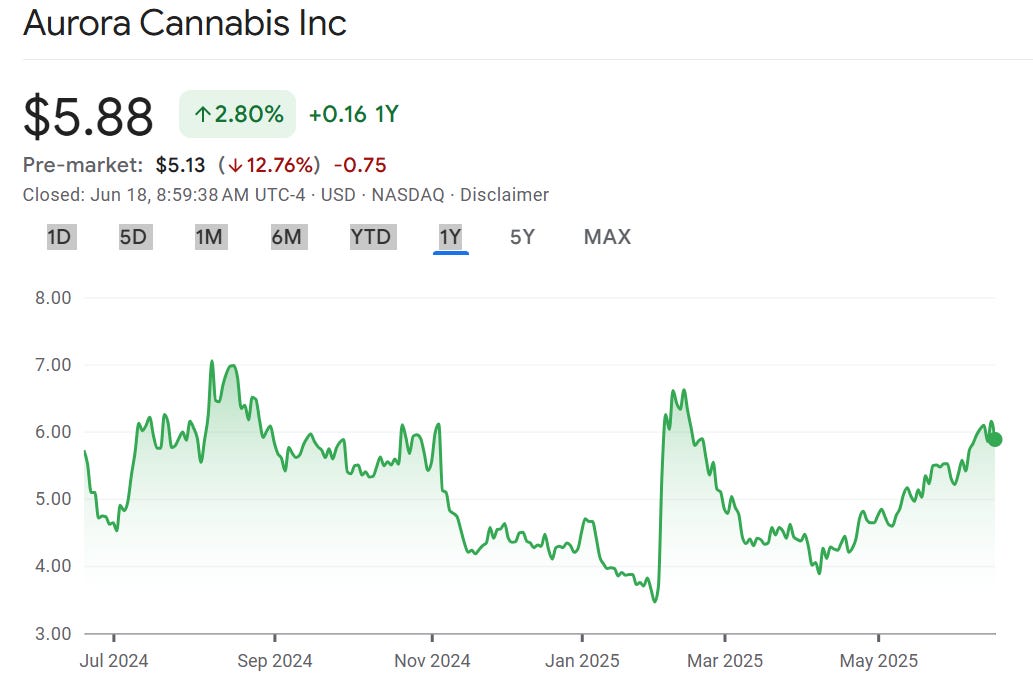

Buzz kill: Shares of Aurora Cannabis are plunging 13% in the pre-market after profit and recreational revenue missed expectations. The marijuana producer said it prioritized its medical cannabis business over its recreational business which lead to a 20% drop in sales there. Medical cannabis, which is a much larger part of their business, grew 48%. Shares have actually done decently well so far this year, up nearly 40% in 2025 (just don’t look at a long-term chart).

Something to marvel at: Shares of Marvell are popping 5% in the pre-market following an AI related presentation yesterday. The chipmaker has been plodding along it’s strategy of supplying chips enable data centres. The presentation convinced analysts they are on the right track. Marvell has been in the penalty box this year after a meteoritic rise last year. “(Marvell), presented a compelling and sustainable growth strategy for its AI datacenter networking/ASIC business,” wrote JP Morgan’s Harlan Sur who also noted multiple customer wins, “Bottom line, if the team can execute to its datacenter growth strategy,” then there is “significant upside in the stock from current levels,” Sur wrote. Their price target is $130/share which implies 85% upside from here.

Withdrawal: Shares of UBS are under pressure after Morgan Stanley cut the stock to sell on the back of potential regulatory changes in Switzerland. New bank capital proposals will constrain future earnings and stock buybacks according to Morgan Stanley’s Guilia Miotto. She believes UBS will continue to underperform European banks. Indeed, European banks have been on a tear up 53% over the past year compared to just 4% for UBS. And just buy the way, they’ve also been outperforming the Magnificent 7!