Pro Picks: Crash Coming? 3 Bold Ideas

Investment ideas from Dan Niles of Niles Investment Management

Pro Picks: 3 Ideas for a Nervous Investor

In this episode of In the Money with Amber Kanwar, Dan Niles of Niles Investment Management says a 50% drop in stocks is on the table. He’s no permabear, he has spent a nearly 30-year career investing in tech stocks - his experience is what is making him cautious. With the S&P 500 overvalued at 24x earnings and double-digit earnings growth expectations looking unrealistic, he advises managing market exposure carefully. Rallies of 18-21% (like those during the tech bubble) can mask broader declines, and he expects volatility ahead. His heavy cash allocation and focus on defensive names like Cisco and Microsoft reflect a strategy to navigate an extended, risky market environment

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB's Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information

Investment Idea #1: Cash (Money Market Funds)

Why It’s a Pick: Niles ranks cash as his top pick for 2025, reflecting his bearish market outlook. With the S&P 500 up 17% from its April 8th lows, he sees limited upside and significant downside risk. Cash in money market funds offers safety and flexibility to capitalize on market dips, which he expects to yield 10-14% bounces on average.

Key Insight: Niles dynamically adjusts his cash allocation, holding more during market highs (like now) and less after corrections, as seen in early April. This approach underscores his focus on capital preservation in an overvalued market.

Actionable Takeaway: Increase cash holdings via money market funds to stay nimble, especially as market rallies extend beyond fundamentals.

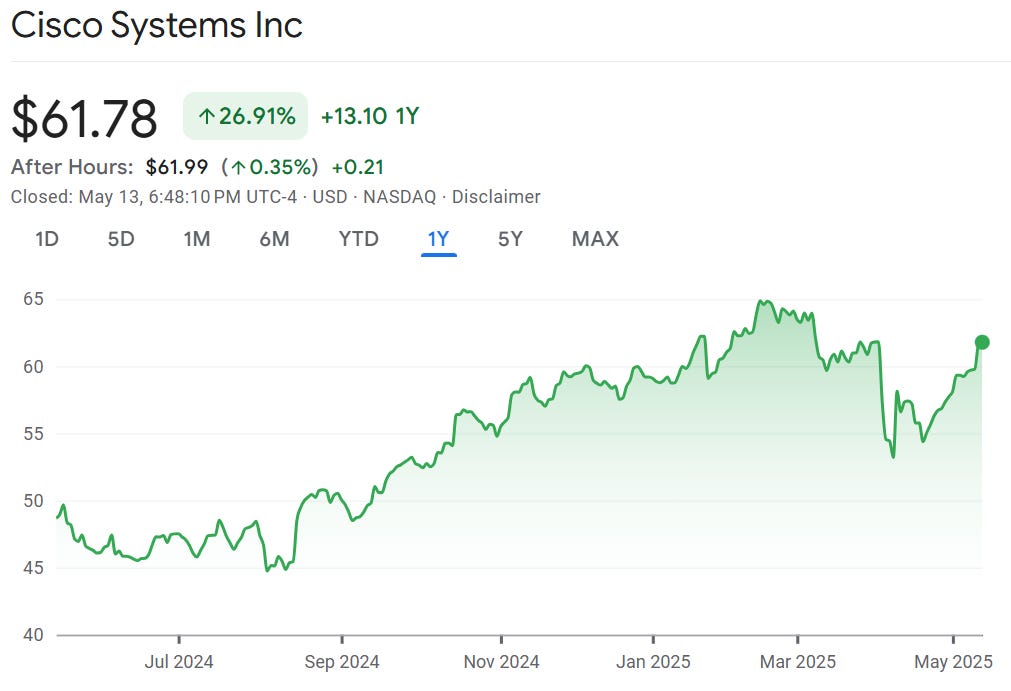

Investment Idea #2: Cisco Systems (CSCO)

Why It’s a Pick: Niles sees Cisco as a standout in the tech sector, poised to benefit from a shift in AI-related spending from infrastructure to networking. As corporations prioritize moving and accessing AI-generated data, Cisco’s networking solutions are well-positioned for growth. The stock trades at a high-teens multiple (below the S&P’s 24x), offering room for multiple expansion if estimates rise.

Key Insight: Cisco is “forgotten” by investors, not yet seen as an AI play, which creates opportunity. Recent quarters have been strong, and Niles expects continued momentum as companies reinvest in network upgrades after years of underinvestment.

Actionable Takeaway: Consider Cisco for long-term outperformance, especially if networking gains traction as a critical AI enabler. Its low multiple and potential for estimate increases make it a compelling pick even in a tough market.

Investment Idea #3: Microsoft (MSFT)

Why It’s a Pick: Among the Magnificent Seven, Niles favors Microsoft for its improving fundamentals and disciplined spending. After three quarters of declining estimates, Microsoft’s recent quarter showed rising numbers and Azure growth acceleration (31% to 33% year-over-year), outperforming competitors like Google Cloud and AWS. Reduced capital spending, now aligned with mid-teens revenue growth, enhances profitability.

Key Insight: Microsoft’s turnaround from the worst-performing Mag Seven stock last year to the best this year reflects operational improvements and market recognition of its AI-driven cloud strength. Niles sees it as the most attractive long-term play in the group.

Actionable Takeaway: Allocate to Microsoft for its solid fundamentals and potential to sustain outperformance, especially as cloud and AI demand grow.

Bonus Pick: NVIDIA (NVDA) – Short-Term Trade Only

Why It’s a Pick: Niles highlights NVIDIA as a potential short-term trading opportunity, not a long-term hold. A $5.5 billion write-down could boost margins temporarily, and strong chip demand (driven by export control fears) may support near-term results. However, he’s skeptical of the back half of 2025, doubting NVIDIA can sustain 10% sequential revenue growth projections.

Key Insight: Niles’ bearish lean is evident here—he views NVIDIA’s current strength as fleeting, with risks emerging later in the year. The stock’s recent underperformance relative to peers suggests investors may already be questioning its AI-driven valuation.

Actionable Takeaway: Consider NVIDIA for a tactical trade ahead of its next earnings, but be prepared to exit quickly, as Niles warns of challenges in the second half of 2025.

DISCLAIMERS: The information provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.